Introduction

Across the United States and around the world, governments increasingly rely on payments for environmental services (PES) to promote conservation on private property. Rather than mandating land-use outcomes through regulation, PES programs use voluntary incentives—compensating landowners who agree to preserve open-space amenities like habitat, watersheds, and working landscapes.

In the U.S., the most prominent PES tool is the permanent conservation easement. Through easements, landowners voluntarily give up development rights in exchange for tax benefits or cash payments—largely from federal or state programs—ensuring land remains conserved. Today, conservation easements cover roughly 38 million acres across the United States, playing a central role in maintaining farms, ranches, wildlife habitat, and scenic landscapes.

Despite bipartisan popularity, conservation easements face persistent criticism, with two concerns most prominent. First, easements may subsidize landowners who would have conserved their land anyway, raising questions about cost-effectiveness. Second, because easement donations are rewarded through income tax deductions, the system tends to favor high-income landowners who can most fully leverage those tax benefits. This can skew participation away from working landowners and communities where development pressure, and conservation value, is often highest.

This research asks a simple but important question: Can conservation incentives be designed to be both more equitable and more effective without increasing public spending? Specifically, it examines how allowing markets for transferable tax credits—a policy adopted by a handful of states—changes who participates in conservation easements and which lands are ultimately enrolled.

How Transferable Tax Credits Create Incentives

Most states mimic the federal income tax code, which treats conservation easements as a charitable deduction that can only be used by the landowner who makes the donation. If that landowner has low or moderate income, much of the tax benefit may go unused or take years to realize. The inability to fully realize the tax benefit effectively raises the price, or cost, of conservation to these landowners. It can make conservation through easements financially unattractive even when the land has high ecological or agricultural value and faces development pressure.

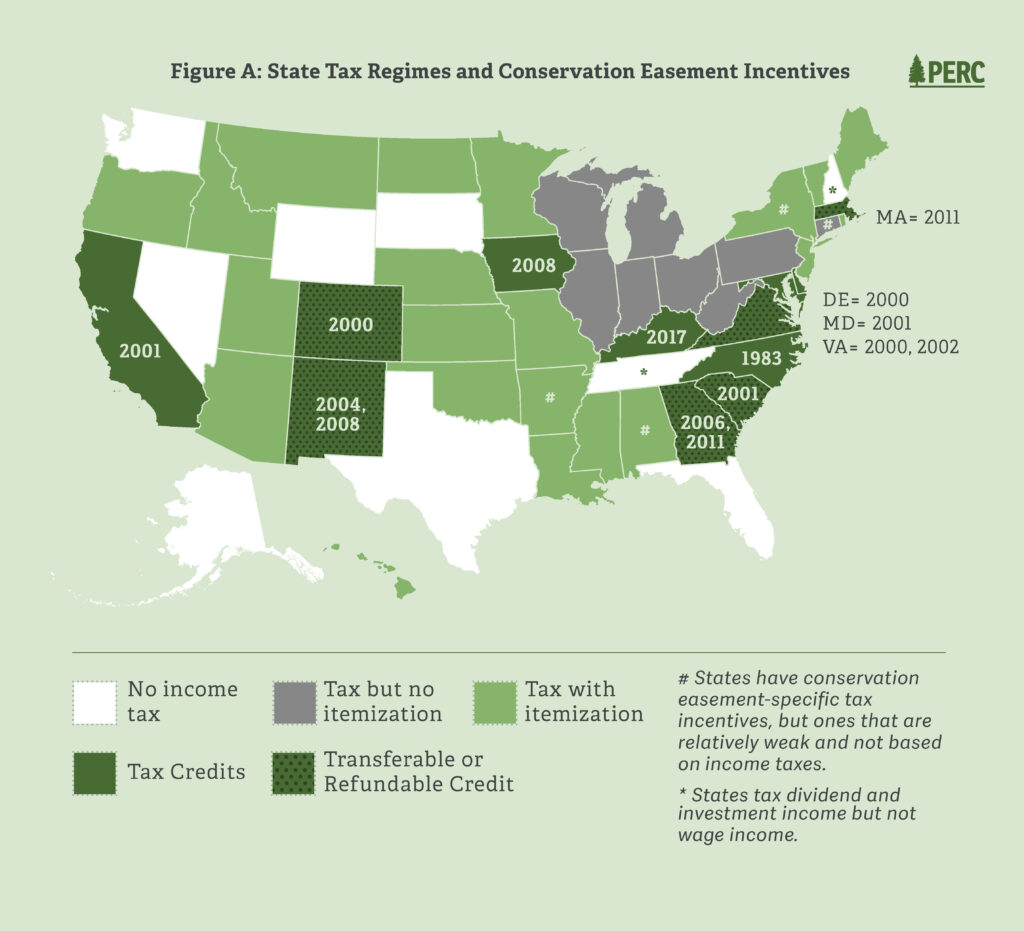

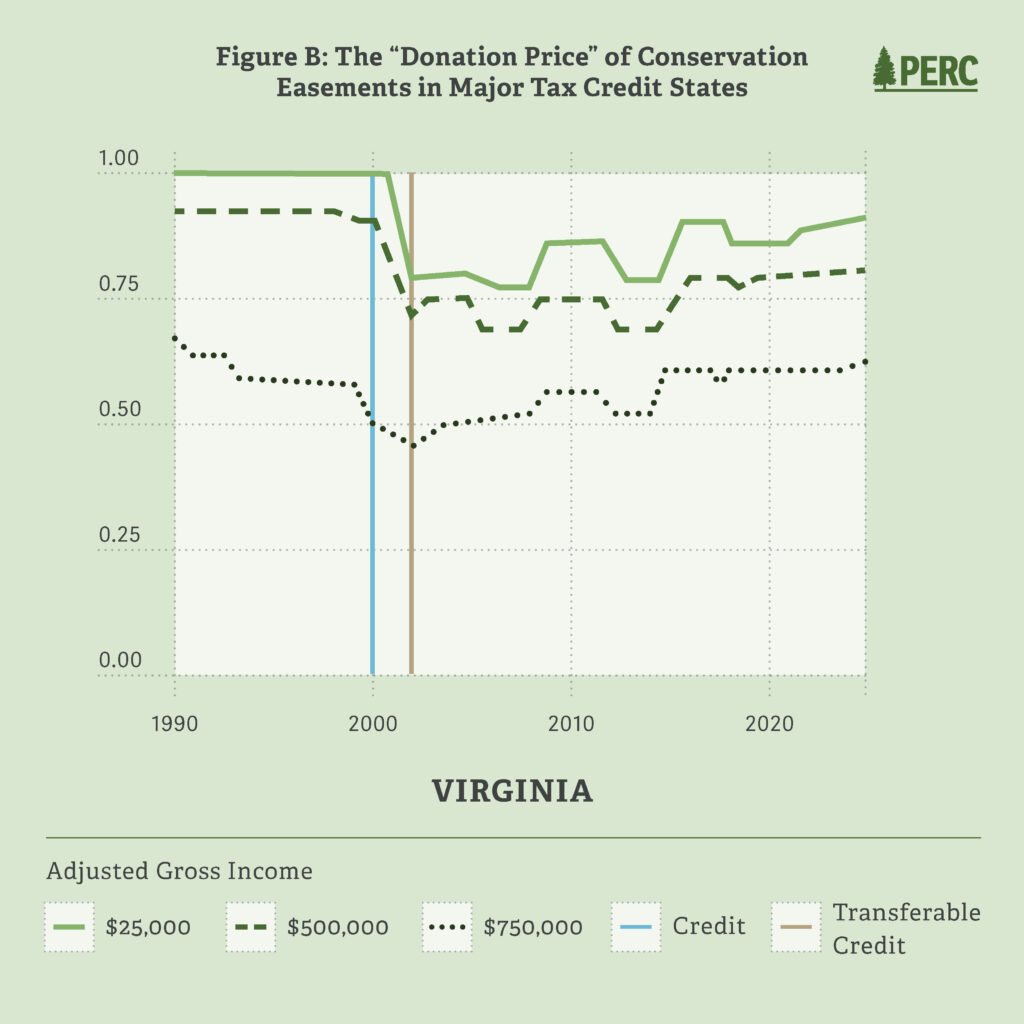

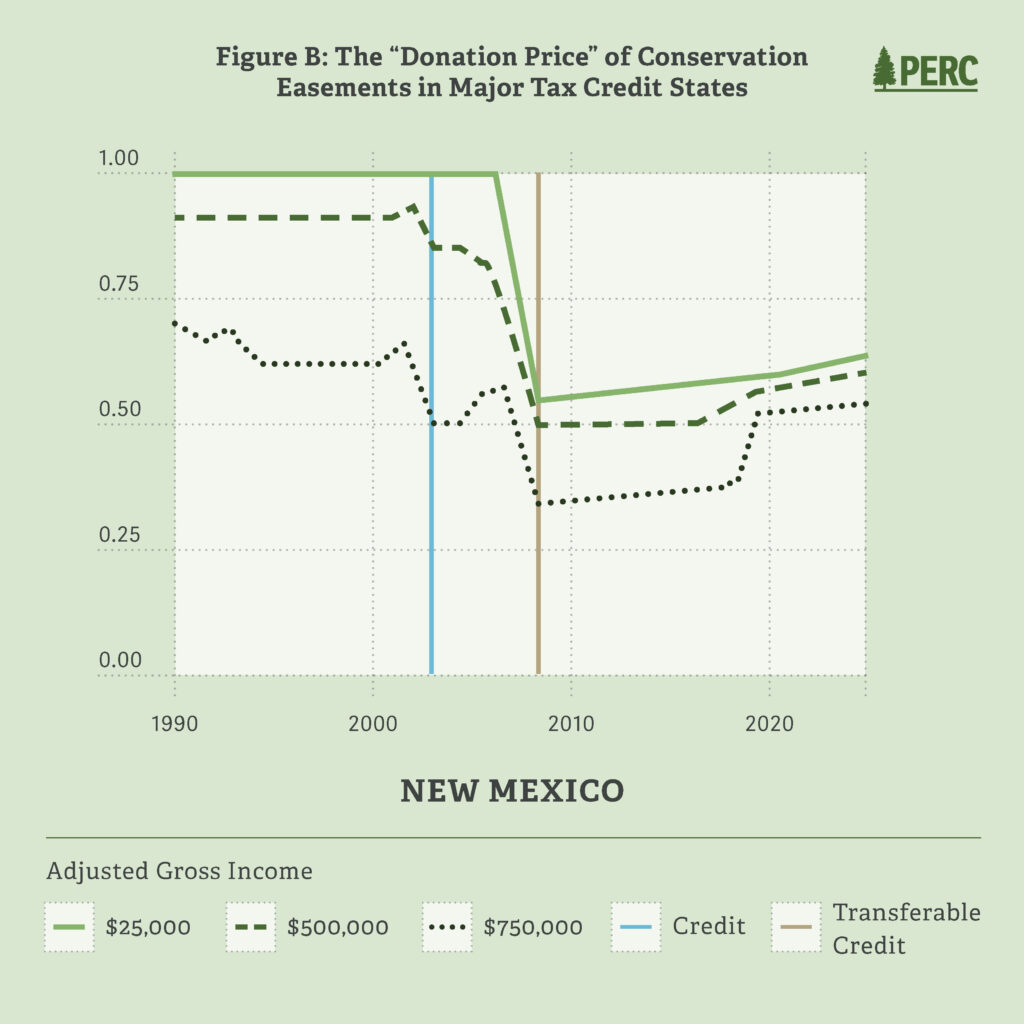

Transferable tax credits change this equation. When credits can be sold, landowners who lack sufficient tax liability can convert conservation value into cash by selling credits to other taxpayers who can use them. In effect, transferability creates a market that links conservation opportunities with those best positioned to finance them. Five states have adopted transferability for tax credits from conservation easements: Colorado, Georgia, New Mexico, South Carolina, and Virginia. (In addition, such tax credits are refundable in Massachusetts, meaning a donor in that state receives a cash payment if the value of eligible credit exceeds the donor’s state income tax liability.)

To understand how this policy shift matters in practice, our Trading Green research combines a detailed calculator of federal and state tax codes from 1990–2025 with evidence from 12 states that adopted and changed conservation tax credits over this period. The analysis specifically examines who donates easements, where those easements are located, what is the ecological and agricultural quality of the areas those easements cover, and how outcomes change once tax credits can be traded.

Dates indicate when the initial tax credit legislation was first in force. For states with multiple years, the first year indicates initiation of a tax credit, and the second year indicates initiation of transferability. New Jersey does not in general allow itemized deductions, but began to allow itemization of conservation easements in 2000. The Massachusetts program is refundable but not transferable. California’s program has operated intermittently since 201. North Carolina’s program was suspended in 2013 and reinstated in 2025.

# States have conservation easement-specific tax incentives, but ones that are relatively weak and not based on income taxes.

*States tax dividend and investment income but not wage income.

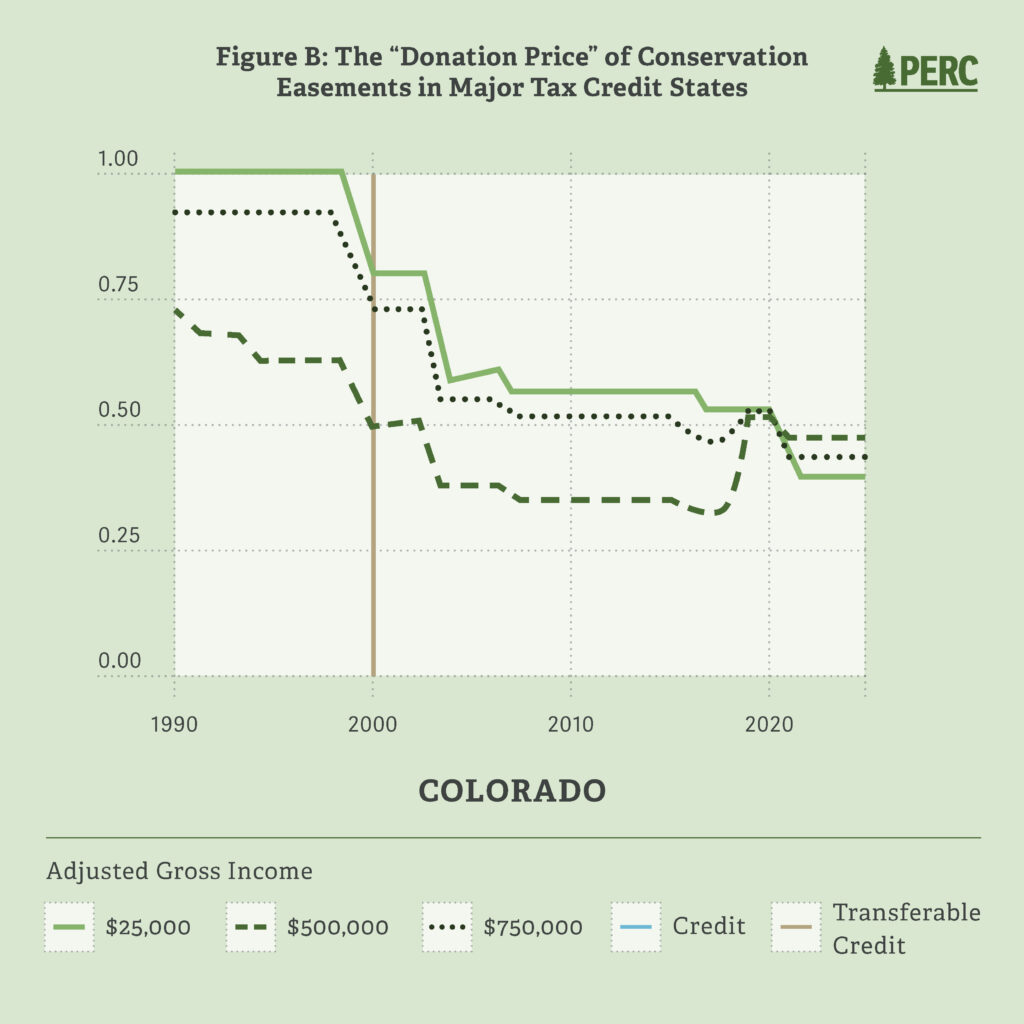

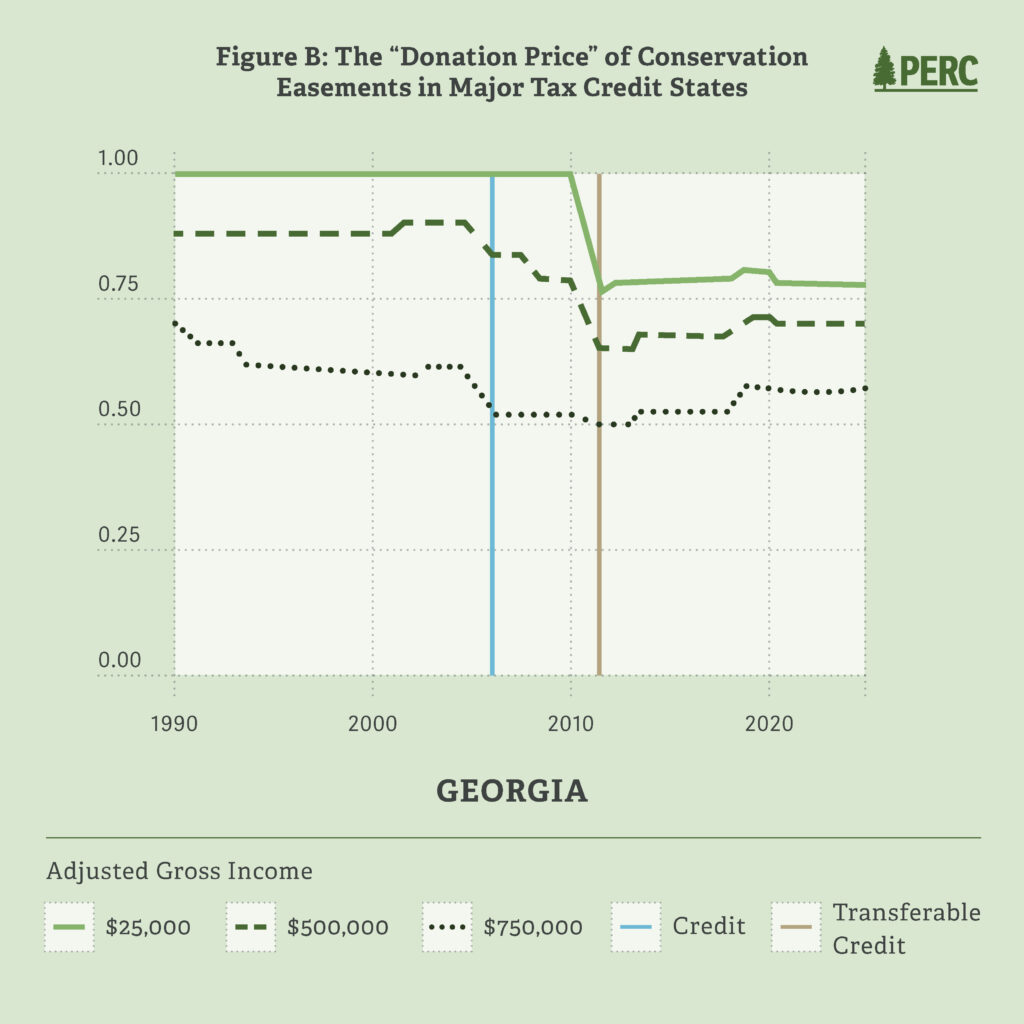

The tax calculator shows how much of an easement donation’s value is recovered through federal and state income tax savings under different scenarios. It generates a value between 0 and 1 that we call the “donation price” of conservation. For example, if a landowner donates an easement valued at $1 million and recovers $300,000 in tax savings, the donation price is 0.7:

1 − $300,000 / $1 million = 1 − 0.3 = 0.7

The lower the donation price, the stronger is the financial incentive to donate.

The tax calculator shows how traditional federal and state treatment of charitable deductions make it much more expensive for low-income landowners to donate a conservation easement as compared to high-income donors. In states that introduced non-transferable tax credits, on average, high-income donors realized a 16 percent increase in the benefit of donating an easement, while low-income donors realized no increase. Compare that to states where tax credits were made transferable: Low-income donors realized a 30 percent tax benefit, while high-income donors realized less than half that benefit.

In addition, we estimate that introducing non-transferable credits increased the annual quantity of easements donated in a state by an average of 34 percent among high-income donors but did not increase the quantity among low-income donors. Adding transferability boosted the response from low-income donors to within 15 percentage points of high-income donors.

Consistent with this pattern, transferability increased the proportion of easements over working farm and ranchlands, and it also reduced the average distance between properties under easement and owner address. Both findings suggest that transferability increased the likelihood that conserved lands remain occupied by local farmers and ranchers rather than by non-local second-home owners. We also find that transferable tax incentives are associated with easements on lands with higher average measures of agricultural soil quality and ecological value.

Research Highlights

1. Before transferability, conservation incentives were skewed toward the wealthy.

High-income landowners faced a significantly lower effective cost of donating conservation easements than low- and middle-income landowners. This disparity limited participation and narrowed the pool of conserved land.

2. Transferable credits level the playing field.

Allowing credits to be sold substantially reduced the gap in effective conservation costs across income groups. Donation responses became far more similar among low-, middle-, and high-income landowners

3. Working lands benefited most.

After transferability, conservation easements were more likely to cover farms and ranches, particularly those facing high development pressure—lands that are often central to both conservation and rural livelihoods.

4. Conservation became more locally rooted.

Transferable credits increased the likelihood that conserved land was owned by local residents, rather than absentee landowners.

5. Environmental outcomes improved.

Easements enacted under transferable credit regimes were more likely to cover land with higher agricultural soil quality and greater ecological value, suggesting better targeting of conservation resources.

6. Quality land trusts are more involved.

The proportion of easements held by land trusts accredited by the Land Trust Alliance increased with transferability, suggesting tax credit markets funnel easements to organizations with high standards of stewardship.

Transferability in Practice

While the core findings of this research are quantitative, the real-world effects of transferability are easy to see by examining how state programs changed once credits became transferable. Across states that adopted transferability, similar patterns emerge: broader participation, more working lands conserved, more participation from the best conservation organizations, and better alignment between conservation value and financial incentives.

Opening the door for cash‑constrained landowners.

In states such as Colorado and Virginia, transferable conservation tax credits made it feasible for family farmers and ranchers to donate easements even when they lacked the income needed to use large tax deductions themselves. Rather than waiting years to realize the value of a deduction, or forgoing conservation altogether, these landowners could sell credits to willing buyers and reinvest proceeds directly into their operations.

Redirecting conservation toward pressured working lands.

Several states saw a shift in the types of lands conserved after adopting transferability. Easements increasingly covered farms and ranches facing strong development pressure, rather than primarily recreational or estate properties. In practical terms, this meant conservation dollars flowed toward landscapes where conversion risk away from agriculture was higher.

Keeping conservation local.

Transferability also reduced reliance on high‑income, absentee donors. In states with active credit markets, conserved lands were more likely to remain in the hands of local owners with closer ties to the community.

Improving ecological targeting without new mandates.

None of these shifts required tighter regulations or more prescriptive conservation rules. Instead, market trade in credits naturally steered participation toward parcels with higher agricultural soil quality and ecological value, as buyers sought credits associated with legitimate, well‑vetted easements. The market reinforced, rather than replaced, existing conservation standards.

Together, these state experiences illustrate how transferability works not as a subsidy expansion, but as an incentive redesign: one that allows conservation value, rather than tax liability, to determine who can participate.

Relevance for Conservation Policy

These findings show how transferability can strengthen voluntary conservation easement programs. By making tax benefits liquid and tradable, transferable credits can expand participation without increasing public spending. They help ensure that conservation decisions are driven less by a landowner’s tax bracket and more by the conservation value of the land itself.

For land trusts and conservation organizations, this matters on the ground. Transferability can make easement projects viable for landowners who are conservation-minded but cash-constrained. Buyers of credits benefit by reducing their tax liabilities, allowing them to invest or spend the savings to drive other economic output, while simultaneously spurring positive conservation outcomes. For policymakers, it offers a way to improve both equity and environmental performance while preserving the voluntary nature of PES programs.

Markets Provide Win-Win Results

Conservation easements remain one of the most important tools for encouraging landowners to continue to produce environmental benefits on private lands in the United States. But their success depends on how incentives are structured. Our research shows that markets for transferable tax credits can make conservation incentives more accessible and more effective at the same time.

By equalizing participation across income groups, steering conservation toward high-value working lands, and improving ecological targeting, transferability aligns private conservation decisions with broader public goals. In doing so, it offers a practical path forward for states seeking to conserve land in better places with broader community support.

In short, “trading green” means providing incentives that work better for individuals, communities, land, and the environment.

For the full analysis, see: Annalise Helm, Dominic Parker, and Garrett Shost, “Trading Green: Do Tax Credit Markets Improve Land Conservation?” working paper, February 24, 2026.